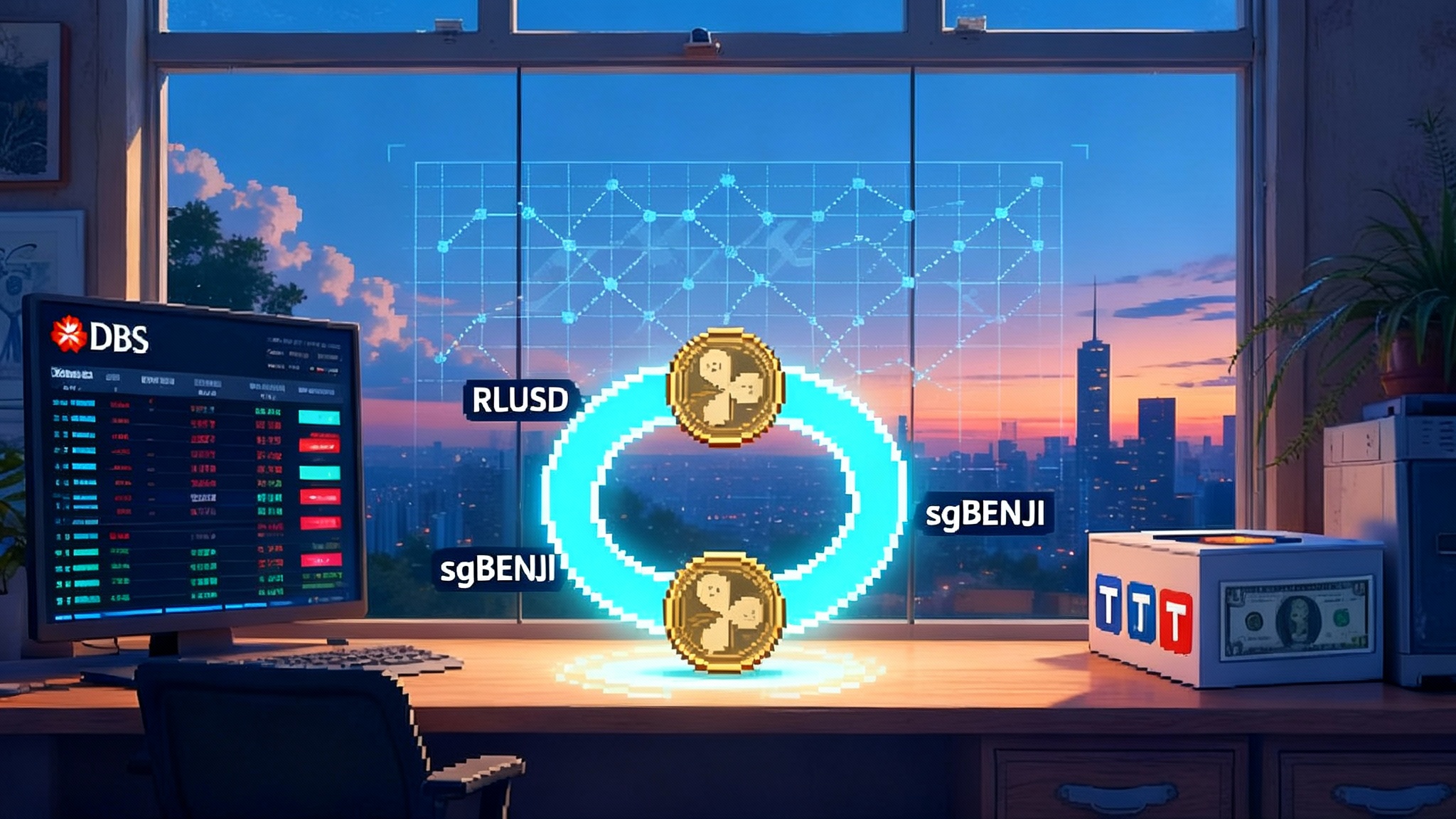

DBS brings sgBENJI and RLUSD to XRPL for 24/7 money markets

DBS is listing Franklin Templeton’s sgBENJI tokenized money market fund alongside Ripple’s RLUSD on the DBS Digital Exchange, creating a bank-grade loop between stablecoin liquidity and yield with repo next. Here is why this 24/7 rail on XRPL could be the template for on-chain money markets.

What DBS, Franklin Templeton, and Ripple just turned on

On September 18, 2025, DBS confirmed that it will list Franklin Templeton’s sgBENJI tokenized money market fund on the DBS Digital Exchange alongside Ripple’s RLUSD dollar stablecoin. Accredited and institutional clients will be able to trade between the two directly, creating a bank-curated rail that connects cash-like stablecoin liquidity to a yield-bearing fund token. The plan includes using sgBENJI as repo collateral or in credit facilities managed by DBS. Franklin Templeton will issue sgBENJI on the public XRP Ledger. The core details were disclosed in the original Reuters report on DBS and Ripple.

A quick map of the rail:

- RLUSD acts as the cash leg for instant settlement.

- sgBENJI represents interests in a U.S. dollar money market fund tokenized by Franklin Templeton.

- DBS Digital Exchange provides matching, custody, and KYC perimeters for accredited and institutional clients.

- XRP Ledger is the shared settlement layer for token issuance and movement, available around the clock.

- Next step is repo and collateralization, with DBS signaling bank-run repo and the option for tri-party style arrangements where DBS acts as collateral agent. Those plans are spelled out in the DBS newsroom release on sgBENJI.

Why issuing sgBENJI on a public chain matters

Most tokenized fund pilots have lived behind walled gardens, which fragments liquidity and constrains interoperability. Issuing sgBENJI on the public XRP Ledger changes the physics of settlement and access in four material ways.

1) Neutral, always-on settlement

The XRP Ledger is a public, neutral network with built-in payments and simple asset issuance primitives. Issuing sgBENJI there gives the fund token an addressable, 24/7 settlement rail rather than a private registry that only tallies positions at end of day. A repo unwind at 03:00 Singapore Time is as mechanically feasible as a trade at 11:00 New York, subject to venue hours and KYC rules. Operations teams can schedule corporate actions and rebalancing around the clock without relying on batched windows.

2) Interoperability by design

Public-chain issuance opens the door for multiple gateways, custodians, and venues to integrate the same instrument. It becomes easier to stitch together a consistent post-trade flow across different institutions because the token’s state lives on a common ledger. This does not erase KYC or transfer restrictions that the issuer may enforce, but it reduces reconciliation work and enables standardized APIs for pricing, margining, and settlement.

3) Settlement transparency

On-chain movements produce an auditable trail. Even if wallet-level privacy is preserved and transfers are permissioned, regulators and auditors can verify issuance, redemptions, and aggregate flows with less manual work. This can improve time to close and reduce disputes around cutoffs once repo and derivatives reference these tokens.

4) Composability with other XRPL-native rails

XRPL supports simple order books and automated market making. Over time, that makes it straightforward to quote RLUSD to sgBENJI pairs, build time-weighted execution, or create hedges around settlement windows. Tokenized collateral and a cash leg that already live on the same ledger can slot into margin engines or netting layers with lower integration cost.

A stablecoin to RWA loop that looks like an on-chain money market

The structure DBS is standing up looks like a basic blueprint for an on-chain money market:

- Cash in: Clients hold RLUSD for liquidity and payments. RLUSD behaves like on-chain cash with clear reserve rules and enterprise distribution.

- Yield on: When clients want yield, they swap RLUSD into sgBENJI. That allocates into short-dated government money market exposures that track prevailing rates.

- Collateral out: Clients can pledge sgBENJI as collateral to raise RLUSD or fiat credit via repo. DBS acting as collateral agent means traditional credit lines can reference a tokenized asset without reinventing tri-party mechanics.

- Loop and net: The same loop can power intraday or overnight liquidity. Firms can source RLUSD against sgBENJI in the morning, unwind at day-end, or roll positions, just as they do with T-bill repos. All of it is timestamped and settled on a shared ledger.

This is not only about convenience. When the cash leg and the collateral leg share a settlement substrate, operational risk drops. No waiting on ACH files, no wire cutoffs that mismatch cash and collateral legs. That convergence is the essence of money markets going on-chain.

Why this is a blueprint rather than just a listing

- It creates a bank-operated venue for a risk-free rate proxy. Tokenized government money funds can be the on-chain analog to the traditional sweep account. RLUSD provides the cash bridge. Together they form a programmable cash and collateral stack that institutions recognize.

- Repo is the forcing function. Once repo exists against sgBENJI with clean tri-party attestations and clear legal agreements, other lenders and borrowers can price term structures and haircuts. That is how a real money market takes shape.

- Public-chain issuance ensures the rail is not locked to a single custodian or message bus. If another bank wants to join, it does not need a parallel registry. It can plug into the same token and settle on the same layer, subject to permissions.

Implications under the new U.S. stablecoin law

The GENIUS Act, signed on July 18, 2025, provides a federal framework for payment stablecoins. It requires 1:1 liquid reserve backing, monthly public reserve disclosures, and licensing for issuers, with a split of federal and state oversight based on scale. It also clarifies that compliant payment stablecoins are outside the securities or commodities buckets and gives holders priority claims over reserves in insolvency. The law goes live the earlier of 18 months after enactment or 120 days after final rules, with service providers getting a transition window into 2028.

Within that context, this DBS rail signals three things.

- For USDC and Tether: Bank-grade rails will favor the most transparent, regulated cash legs. As banks implement counterparty and concentration limits that reference the new law, liquidity providers may prefer compliant stablecoins for institutional rails. This may not change retail trading dynamics, but it channels institutional flow toward fully regulated stablecoins.

- For banks: The law removes a major excuse. With a clear federal framework, banks can hold, distribute, or even issue stablecoins subject to prudential rules. A bank that can pledge tokenized funds against a permitted stablecoin on a shared ledger can shrink settlement windows in its treasury stack. Expect peers to replicate the DBS loop with other stablecoins and tokenized funds.

- For DeFi treasuries: The message is to get compliant or get cordoned off. Treasuries that satisfy KYC and onboarding will be able to park reserves in tokenized money funds on public chains and source liquidity against them. Those that cannot will sit in a parallel market with less institutional depth. The incentive to adopt permissioned wrappers, on-chain KYC proofs, or regulated custody will rise.

For more on stablecoin distribution dynamics, see MetaMask mUSD and the distribution war.

Why XRPL, and what about chain risk

DBS and Franklin Templeton did not pick XRPL at random. The ledger has low fees, predictable finality, and a long-standing model for issued assets. It also has built-in exchange features for quoting and routing between assets. For a bank that wants to run a curated loop between a cash token and a fund token with minimal moving parts, XRPL is a strong fit.

That said, chain choice is a real risk. Ethereum, Stellar, Polygon, and others already host tokenized funds. Liquidity can fragment if the same issuer is present on multiple chains and if venues do not bridge properly. Institutions will push for either uniform issuance on one chain per instrument or for standardized cross-chain attestations and atomic settlement. For a view on consolidating liquidity, compare AggLayer and unified multichain liquidity.

The competitive posture for RLUSD

RLUSD positions itself as an enterprise-grade stablecoin with distribution through payment networks and exchanges that serve institutions. Being paired with sgBENJI on a bank’s exchange is an immediate credibility boost. The question is whether RLUSD can win bank desks and corporate treasuries that already use USDC. Under the new law, differences will come down to reserve composition, transparency, market depth, and integrations with bank-grade venues.

In the short run, the most likely outcome is multi-stablecoin support. Banks will curate two or three permitted stablecoins and let customers pick. Over time, the cash leg that offers the best liquidity in repo and the tightest spreads into tokenized T-bill or MMF rails will dominate. If RLUSD becomes the cheapest path into and out of tokenized government funds on XRPL, it will earn flows.

For cross-border policy context on tokenization, see Hong Kong tokenization ambitions.

Risks and open questions

- Custody and key management: Tokenized MMFs and stablecoins require secure custody. Keys can be compromised, and operational errors can freeze assets. Clients need clarity on segregation, insurance, and recovery.

- KYC perimeters and transfer controls: DBS Digital Exchange is for accredited and institutional investors, and issuers can impose transfer restrictions. That limits organic network effects but is necessary for compliance. The challenge is designing allow-lists that still let multiple banks interoperate.

- Chain choice and vendor risk: XRPL is fast and stable, but any public chain carries protocol, governance, and upgrade risks. Institutions will want clear incident response playbooks and legal agreements that allocate chain-related losses.

- Liquidity fragmentation: sgBENJI on XRPL is powerful, but if other banks tokenize rival MMFs on other chains, price discovery could splinter. The market will need cross-chain settlement standards or common gateways that eliminate basis risk.

- Regulatory harmonization: The rail sits at the junction of Singapore rules, U.S. fund law, and the new U.S. stablecoin statute. Cross-border distribution, tax treatment, and accounting can complicate adoption unless regulators align on reporting and capital treatment.

Adoption signals to watch next

- Exchange volumes and spreads: Track RLUSD to sgBENJI volumes and quoted spreads on DBS Digital Exchange. Tight, deep markets are the best evidence that the loop works for real treasury flows.

- Repo pilots: Watch for announcements of term sheets, eligible collateral schedules, and haircut grids for sgBENJI-backed repo. The moment another bank or a large broker-dealer joins as counterparty, the market will take notice.

- Custody integrations: If major custodians add native XRPL support for sgBENJI and RLUSD with full policy controls and reporting, onboarding friction falls sharply.

- More fund families: Look for other asset managers to tokenize government funds on XRPL or commit to interoperable issuance across chains. A second or third issuer would validate the blueprint.

- U.S. institutional access: Once the stablecoin law rules are finalized, expect U.S. banks and fintechs to announce permitted stablecoin support and tokenized cash products. If they mention direct support for XRPL-issued fund tokens, the network effect accelerates.

- On-chain holder metrics: Even with transfer controls, growth in the number of qualified wallets holding sgBENJI on XRPL will indicate genuine adoption rather than announcement theater.

The bottom line

The DBS - Franklin Templeton - Ripple rail is more than an exchange listing. It is a working circuit between a bank-curated cash token and a tokenized money fund that lives on a public ledger, with repo up next. That is what an on-chain money market looks like. It should compress settlement risk, standardize collateral flows, and pull institutional liquidity onto a shared substrate that runs all day, every day. If repo proves out and more banks and issuers plug in, this will look obvious in hindsight. Today it looks like a credible template for how stablecoins and RWAs meet at bank scale.