States vs. PJM: Data Centers Ignite a Governance Clash

AI demand and spiking capacity prices have jolted the Mid-Atlantic. Governors are challenging PJM’s authority, pressing for control over who pays, who builds, and which market rules will reshape the grid. Here is the playbook for the next two years.

The spark: capacity prices jump as AI demand soars

Through most of the 2010s, PJM was known for ample reserves and low prices. That flipped when the 2026 to 2027 capacity auction cleared at the Federal Energy Regulatory Commission price cap across the footprint. The result shocked governors and public utility commissions accustomed to soft outcomes. PJM cited an influx of new demand, a backlog of projects, and a wave of retirements as core drivers. The clearing result reframed Mid-Atlantic politics and armed state leaders pressing for change, landing exactly as AI and cloud operators scoured the region for megawatts. See the PJM auction summary.

The governors step in

In late September 2025, Virginia Governor Glenn Youngkin and Pennsylvania Governor Josh Shapiro led a cohort of Mid-Atlantic governors calling for more state control over how PJM plans and prices the grid. Their message blended reliability concerns, rising retail bills, and sudden data center load. They did not rule out drastic options, including the possibility of exiting the regional transmission organization if governance does not evolve to reflect state priorities. Even raising that option is both a negotiating tactic and a policy marker.

What actually changed inside PJM

Three forces converged at once:

- Load growth from hyperscale computing. New data centers no longer sip power. Individual campuses can demand hundreds of megawatts around the clock, and AI training clusters can push those baseload profiles even higher.

- A supply stack in transition. Retirements of aging coal and older gas units accelerated while interconnection queues lengthened. Renewables and batteries are coming, but not always at the speed or locations that match new load, a dynamic shaped by the 45Y and 48E crunch.

- A planning cadence built for gradual change. When demand curves step up, planning horizons that once looked conservative can suddenly feel stale.

PJM’s capacity market balances these factors through a three-year forward auction that pays resources to be available in a future delivery year. If the system looks tighter, prices rise to pull in supply. The 2026 to 2027 results did exactly that, but the political interpretation differs. Where the market sees a price signal, governors see a bill arriving at households and small businesses already under strain.

The new political math of megawatts

Data centers bring jobs and tax base, yet the electricity math now looms as large as the economic development headlines. Counties welcome investment. Utilities welcome new sales. But if the grid needs new firm capacity and transmission to serve campuses that can approach the load of a small city, the question becomes who pays and when.

That is why a governance debate that once felt esoteric now lands on the front page. Do states get a bigger say in market rules that determine how resources are accredited and compensated. Do they get clearer levers over transmission buildouts that follow the load. Do they have vetoes over siting that may constrain where hyperscale facilities can cluster.

Winners and losers under higher capacity prices

Higher capacity prices alter the investment scoreboard in ways that cut across traditional alliances:

- Incumbent thermal units gain breathing room. Coal and combined-cycle plants on the bubble can clear revenue to fund maintenance and seasonal upgrades.

- New gas peakers look more viable. Fast-start turbines that cover evening ramps and winter peaks gain a clearer business case when capacity is scarce.

- Batteries benefit but with nuance. Storage captures value when accreditation reflects reliability at critical hours. The details of effective load carrying capability move billions of dollars.

- Demand response and load flexibility become strategic. If heavy industrials and data centers can curtail or shift load on tight days, those capabilities can clear capacity and cut procurement costs.

- Nuclear looks steadier. Uprates and life extensions become easier to justify when scarcity rents are visible and durable.

Where utilities land depends on whether they own the assets that win. Where merchant generators land depends on accreditation and performance penalties. Everyone cares about the shape of the next rules.

Market design fights to watch

Several levers inside the capacity market could move next, each with ripple effects:

- Accreditation of intermittent and hybrid resources. Expect continued work on how to credit wind, solar, and storage for reliability at the actual hours of risk, especially winter mornings and multi-day cold snaps.

- Performance in extreme weather. Reforms after winter events tightened penalties and incentives for resources that fail to start. More changes are likely, with sharper carrots and sticks tied to the FERC grid reboot order.

- Seasonal and locational signals. If specific pockets keep getting tight, zonal price separation can intensify, making siting and interconnection choices more consequential.

- The minimum offer price rule debate, rephrased. States that want to procure clean energy may demand procurement paths that do not distort market outcomes, while generators try to prevent policy-driven price suppression.

Each choice answers a reliability question and also decides who captures capacity rents over the next decade.

Governance reset: what states want

States are not asking to micromanage dispatch. They want mechanisms that tie market rules and planning to on-the-ground realities. Three tracks stand out:

- Board and stakeholder balance. Expect proposals that give states more formal weight in PJM’s stakeholder process. That could mean new voting structures or a reinforced role for a state committee in setting priorities and calendars.

- Planning that follows load. Governors want transmission upgrades, interconnection reform, and local deliverability studies that anticipate where data centers will land rather than simply reacting to queues. Better data will matter, including impacts from the EPA 2025 data blackout.

- A clearer exit or carve-out pathway. Even mentioning a departure signals that states want credible alternatives if they believe the market fails to deliver reliability at acceptable cost. The Fixed Resource Requirement pathway exists, but it was designed for a different era.

These are not just governance questions. They are about trust. When load grows in giant steps, states want assurances that reliability will not falter and that costs will be assigned fairly.

Policy experiments to watch

Two strands of experimentation are emerging.

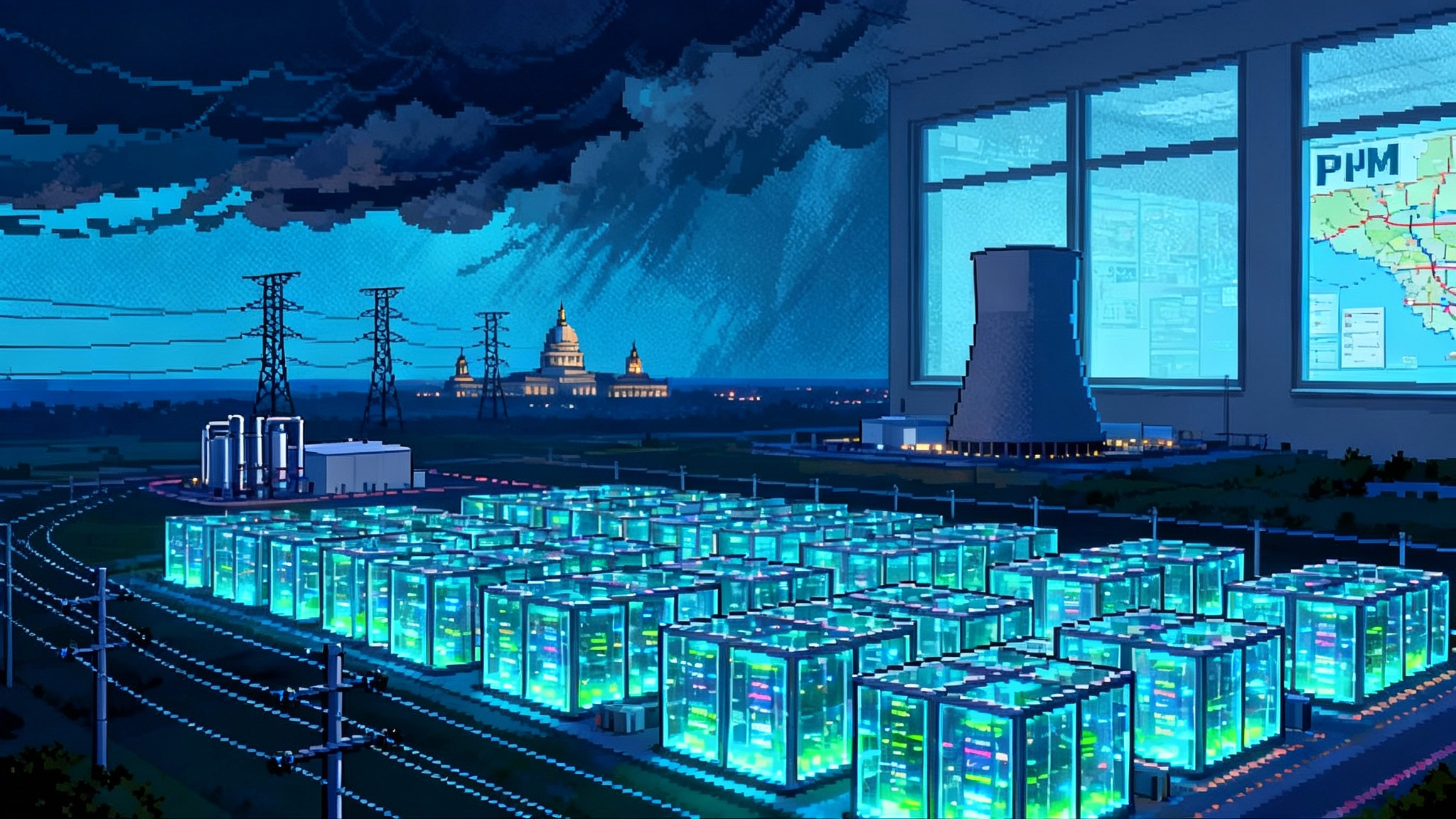

First, utilities are testing rate design that isolates the impact of rapidly growing data center load. Dominion Energy Virginia proposed creating a separate rate class for data centers with pricing that reflects their unique demands on the system. The goal is to shield other customers from cross-subsidies while preserving a pathway for hyperscale growth. The details matter, including how customers qualify, how demand charges are set, and how capacity and transmission costs are allocated. See the Dominion filing on data center rates.

Second, developers and large buyers are exploring dedicated firm generation for data loads. The concept is simple. Build a plant that runs primarily to serve a cluster of campuses and contract the output over long terms. The technology palette ranges from efficient combined-cycle gas to aeroderivative peakers paired with storage and demand response. Some proposals sketch on-site firming resources close to campuses, others envision regional plants that wheel power over dedicated transmission.

A marquee idea is a large gas-fired project built in a region with abundant fuel and delivered under long contracts. The dataset size of AI training runs and the urgency of cloud expansion make long-term offtake more feasible than in the past. If state regulators and PJM can align accreditation and deliverability with such projects, they could reduce pressure on the broader capacity market while preserving reliability.

There are also early-stage conversations about nuclear options. Uprates and life extensions of existing plants are the most practical near-term steps. Small modular reactors remain intriguing for campus-level firming, but timelines and licensing push them outside the urgent window that hyperscale operators face today.

Siting and interconnection: from queue to crane

Governors are zeroing in on the chokepoints between an application and a shovel in the ground. Three themes recur in meetings between state energy offices, utilities, and data center developers:

- Clustered load needs clustered upgrades. Northern Virginia, central Pennsylvania, and parts of Ohio have substation and transmission corridors under strain. Planners will need multi-node solutions that move bulk power and reconfigure local networks.

- Queue reform is necessary but not sufficient. PJM has modernized study processes and prioritized projects with realistic timelines. Even so, the geometry of where new resources connect relative to new load will drive reliability risk. Deliverability tests and local capacity rules will have to adapt.

- Fuel logistics are back on the agenda. If dedicated firm generation is built, accompanying fuel transport needs scrutiny. Gas pipeline capacity and winter reliability planning will shape feasibility and pricing.

Expect states to press for coordinated study clusters around known data center geographies. Expect utilities to seek faster cost recovery of enabling upgrades. Expect developers to pursue staged interconnections as campuses scale.

Rate design and who pays

The fairness debate will hinge on how much of the new grid is built for everyone versus how much is built for specific customers. Rate design tools likely to rise include:

- Dedicated rates for large new loads, with tailored demand charges and cost allocation that follows measurable impact on capacity and transmission.

- Subscription-style tariffs that reserve a block of firm service and price incremental usage at premium rates, paired with incentives for flexible operations.

- Critical peak pricing to reward load that curtails during the rare but expensive hours that set capacity obligations.

- Performance-based credits for quantified flexibility, such as automated demand response that meets telemetry and verification standards.

These tools give regulators levers to protect smaller customers while keeping the welcome mat out for investment. The art is in calibration. Prices must signal real costs without pushing growth across state lines.

Utilities versus IPPs: new lines in old sand

Utilities bring planning responsibilities, franchise obligations, and balance sheets. They can build rate-based generation and wires if regulators agree the investment serves the public. Independent power producers bring development speed, merchant risk appetite, and an ability to contract directly with large buyers.

In a tight capacity environment, both can win. Utilities can secure approvals for strategic upgrades, grid-enhancing technologies, and in some states new firm generation. IPPs can finance fast-cycle projects that clear in capacity auctions and contract with hyperscalers. The contested terrain will be interconnection priority, deliverability metrics, and whether state procurement tilts toward one camp.

Batteries and demand response in a winter risk world

Storage and load flexibility remain the most versatile tools to bridge the next few years. Batteries can soak up off-peak energy and release it during evening ramps. They can also add synthetic inertia and voltage support that keep local networks stable. Demand response can spread the peak and lower the amount of firm generation the market needs to procure.

However, accreditation rules that reflect multi-day winter stress events will determine how much capacity value batteries receive. Longer-duration assets and well-designed aggregation of flexible load will climb in importance. For data centers, that could mean engineered maintenance windows, noncritical workload shifting, and on-site backup that can feed the site during rare system emergencies.

Scenarios for the next two years

- Baseline evolution. PJM sticks with the price signal and accelerates interconnection processing, while FERC and states push for sharper accreditation and performance rules. Prices moderate as new resources clear and dedicated projects advance.

- State leverage. Governors extract concessions on governance and planning, including a formalized role for a state committee prioritizing studies and upgrades. Rate designs that isolate large-load effects become common across the footprint.

- Fragmentation risk. One or more states threaten to exercise FRR-style carve-outs or accelerate bilateral procurement in parallel to PJM. The region avoids a break, but rules adapt to accommodate more state-directed capacity procurement.

Each path leads to a different mix of who builds and who pays, but all assume AI-driven load is not a blip. The grid has entered a new demand era.

What to watch next

- Regulatory calendars. Expect rapid-fire dockets on large-load rates, data center interconnection, and integrated resource plans. Stakeholders should track sequences and align comments across related cases.

- PJM stakeholder meetings. Watch proposals on accreditation, winter readiness, and local deliverability move through committees with unusual speed. The composition of the PJM Board and any governance working groups will signal how far change may go.

- Corporate procurement. Look for multi-gigawatt long-term offtake that blends clean energy with firming resources and explicit flexibility commitments.

- Transmission announcements. Upgrades that unlock data center clusters will be the clearest indicators that politics and markets have found a workable truce.

The headline is not just that capacity prices jumped. It is that a market designed for gradual change is meeting a demand curve that steps upward. Governors are not waiting for another auction to provide direction. They are trying to write the rules now, in full view of voters who will notice when the bill arrives, and in dialogue with companies building the digital backbone of the next economy.